Originally printed in the June 2021 issue of Produce Business.

Nobody really knows what the future for online grocery shopping will be. With the COVID-19 pandemic receding, we can expect that habits developed as a result of the pandemic will also recede — but probably not totally. So, for example, people who avoided public places, such as supermarkets, and bought most food online may feel comfortable shopping again and so will reduce their online purchasing.

Perhaps more importantly, the world changes and this will lead to changes in shopping habits. Children go back to in-person school and so get lunch at school. Parents go back to work and eat lunch out with colleagues. Of course, none of this will be 100%, as some children have done well with home-schooling, and their parents will continue that; some people will be allowed to continue to work from home — maybe 100% of the time or maybe just 20% of the time.

The key point, however, is that higher and higher percentages of food purchases have been made every year in foodservice outlets, and that sector is already rebounding strongly. It would be very surprising if 20 years from now, when we look back at the graph, we didn’t see a continuation of this trend. After all, even changes can have counter-changes. So if people start working from home, they may also start wanting to travel more for business or vacations. They may want to start meeting friends and business associates for lunch. Husbands and wives locked up working in separate bedrooms all day may eat dinner out more frequently just to get out of the house.

The truth is that current technology poses large challenges for innovation among producers. It is not just that it is difficult to market an innovative product online; it is that the number of people even looking is small.

This writer purchased much food online for his family during the pandemic. The thing was… we entered a large order, about $300, then basically reordered it many times. Sure, if someone in the family specifically asked for an item, we would add it, but we didn’t have the time or desire to re-examine that entire order. We just ordered again. The first order took an hour, but, each time after that, it took two minutes.

Anne-Marie Roerink astutely notes that people “start with their past purchases when placing an online order.” It needs to be remembered though that this start is different from shoppers going into a physical store and starting their list with past items. They see other items regardless of what is on their list, whereas online, they may just press a reorder button.

Now this is an issue for all food items… how do you introduce something new and exciting online? But in produce, with seasonal variations, it is a large problem. Especially if, like us, people don’t so much “shop” online for food, as just order.

Perhaps the perfect program for a future will have commodity foods ordered online and consumers left to curate their fresh foods in a new-format retailing environment.

Fortunately, our sense is that the threat from online ordering in produce may be overstated because we suspect a hybrid model will emerge. Consumers may well order online items that are consistent — say a case of Dasani water or cans of Campbell’s Soup or boxes of Tide detergent. Stores may evolve to be smaller and not stock these things, but they will offer plentiful foodservice and fresh foods options.

The foodservice options will bring customers in frequently, and the fresh foods will change regularly. Produce will actually be highlighted more than ever, and foodservice options will increasingly be integrated as they will regularly feature the fresh food being sold in the stores. Indeed, the financial pressure on shippers may be to chip in so the Duck l’Orange becomes the Duck l’Sunkist!

Indeed the produce industry, which is accustomed to commodity sales, may find the need becomes more urgent to invest in product distinction and in recipe development. Fortunately, the investment in new grape varieties paints a picture for the industry of how we can develop products that offer distinct flavor profiles and unique quality attributes. Perhaps the perfect program for a future will have commodity foods ordered online and consumers left to curate their fresh foods in a new-format retailing environment.

Of course, all this may not be the direction the industry most needs to take. After being holed up for over a year, the Roaring 20’s may repeat itself, and the big opportunity may be within the foodservice sector as people decide to celebrate their newfound freedom.

Yet this a challenge too. How does the industry move the foodservice sector away from its overwhelming dependence on PLOT — potatoes, lettuce, onions and tomatoes? How do we get those premium products that are being developed in areas such as grapes to not only be used more in foodservice but to justify premium prices because consumers will prefer to buy more flavorful, and distinctive, dishes and even will be willing to pay a premium for dishes made with such items.

History is rarely linear, and the post-pandemic period will lead to changes unexpected. Our challenge is to make sure those changes lead to more appreciation, and consumption, of fresh fruits and vegetables.

RESEARCH PERSPECTIVE

Grocery E-commerce Opportunity Remains

By Anne-Marie Roerink, President, 210 Analytics

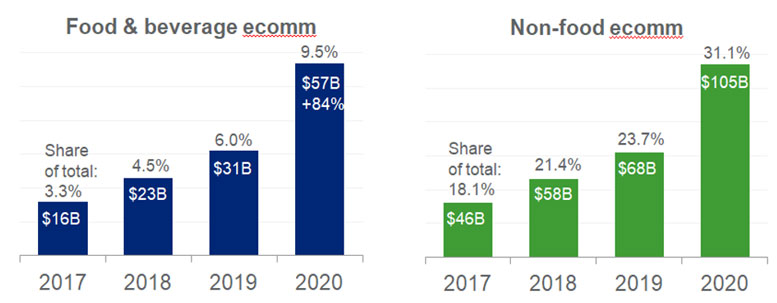

Grocery e-commerce has been an area of growth for many years. In 2017, the online portion of total food and beverage sales was a mere 3.3%. Come 2019, that had grown to 6.0% or $31 billion. The pandemic prompted not only further growth of e-commerce, but a rapid acceleration. By the end of 2020, e-commerce made up 9.5% of all food and beverage sales in the U.S., reflecting annual growth of 84%, according to IRI.

Even so, online food and beverage sales trail non-food by a wide margin. Non-food CPG ecommerce reached $105 billion in 2020, now reflecting 31% of all dollars sold. This signals both an important gap and growth opportunity for food and beverage e-commerce.

E-commerce engagement

The $26 billion increase in U.S. e-commerce sales was based on more people buying online, existing customers buying more each trip and people buying food and beverages online more frequently — the trifecta of growth. In 2019, 47% of consumers had purchased groceries online. In 2020, that share rose to 64%, according to research by 210 Analytics.

However, many shoppers have increased their order frequency over the past year. Online weekly orders rose from 5% in 2019 to 11% in 2020. Likewise, the share ordering every two weeks increased from 4% to 9%. IRI found that among new online shoppers as of the start of the pandemic in March 2020, 50% continue to buy online and about 20% have become heavy hitters. The online basket averages $74 versus $55 for the average in-store ring. Online shoppers are less price-sensitive and spend an average of 13% more per unit online versus offline for fresh foods.

E-commerce fulfillment types

As more retailers dialed up click-and-collect or delivery, ordering through the website of local brick-and-mortar retailers is by far the most popular way to buy food and beverages online. In 2020, 69% of all CPG dollars came by means of a website of a brick-and-mortar retailer. The second-largest share was generated by third-party delivery companies, such as Instacart, at 26% and the remaining 5% came from online-only food and beverage companies. The share generated through the online presence of brick-and-mortar retailers is not only the largest but also increasing. When looking at the same three-way split during just the month of December, 73% of dollars came from the online presence of brick-and-mortar retailers versus just 2% from pure online players.

Subsequently, click-and-collect — where the order is placed online, but the shopper picks up the order at the store — is growing the fastest. Another consequence is a changing basket mix. Due to click-and-collect and the acceleration of e-commerce during the pandemic, the online basket now includes more perishable items, such as meat and produce, with fulfillment by the trusted retailer. Fresh food e-commerce, that had lagged center-store and frozen, grew as much as 200% during the early months of the pandemic.

Brand, or basket, loyalty

More than four in five online consumers (82%) start with their past purchases when placing an online order, according to research by 210 Analytics. The longer someone has ordered online, the more likely they are to start with their favorites. After all, more frequent online orders means a greater level of curation in their past order history. But this also has great consequences as it is resulting in great brand, or perhaps more accurately put, basket loyalty. IRI studied a variety of brands and their share of wallet in store versus online. For each, the online loyalty was significantly higher. This means winning from the first click is crucially important as is having a strategy to create visibility for new items, seasonal offerings and flavor extensions.

The same goes for impulse items. There are many fresh categories that benefit from impulse purchases, such as fruit, floral and baked goods, and driving impulse online in the same vein as inspiring unplanned purchases in-store will be crucial to maintain spending. Brand and retailers have room to close the lost impulse opportunity that IRI places between 0.5% and 1% of omnichannel food and beverage sales by partnering on building baskets to further push underdeveloped impulse categories online.

The who

210 Analytics’ research shows that the core online grocery shopper are the older Millennials and younger Gen X-ers – shoppers right around age 40 who tend to be in their family-rearing and career-building years. With all the demographic changes, the items purchased online are changing too. The early adopters of grocery e-commerce, for example, had a high propensity for health and wellbeing, driving an above-average share of organic, grass-fed and other items consumers associate with health. And at the same time, their focus on saving time spurred above-average shares of convenience-focused items, such as value-added meat and produce. As a result of all of these buying tendencies, branded item sales in the fresh categories is higher online than offline, at +2% for fresh foods overall.

Some crystal ball

While online grocery shopping isn’t for everyone, 79% of those currently doing curbside pick-up and 73% of those who order groceries for delivery expect they will continue to do so the same amount or even more often post-pandemic. This means some shifting back from online trips to in-store, which is precisely what the market has been experiencing in the past few months. But even so, 19% of all trips are still online — vastly higher than pre-pandemic. IRI is expecting continued e-commerce growth, albeit at a bit of a milder pace. IRI anticipates the share of online food and beverage dollars to reach 12% by the end of 2021, up from 9.5% in 2020.

210 Analytics is the brainchild of principal and founder, Anne-Marie Roerink. The San Antonio market research firm’s services include customized market research and data analysis, marketing strategies and public speaking.